.png)

We’ve talked about the liquidity crunch across the banking sector in recent weeks. However, quite a few institutions still find themselves on the flip side of the coin – sitting on too many deposits. Is this a serious problem though? Well, an excess of deposits can negatively impact the health of a bank’s balance sheet. Specifically, an excess can breach regulatory constraints and harm both health and performance metrics.

On the regulatory front, bank growth is limited by capital requirements, which track bank equity capital as a percentage of assets. When deposits grow rapidly, a bank’s capital ratio falls as assets increase yet equity remains constant. To stay compliant with regulation, banks must either shed deposits or raise more capital.

Banks also face regulatory thresholds that are based on asset size. Many fintech banks are incentivized to stay under $10 billion in assets to remain Durbin-exempt and earn healthy interchange revenue from their card programs. Others want to remain under $1 billion in assets to skip additional FDIC reporting requirements, or under $50 billion to avoid the “large and highly complex” designation. Crossing these thresholds often increases the regulatory burden for banks and changes their unit economics.

An excess of deposits can also harm a bank’s health and performance metrics across the board. Excess deposits, by definition, mean the bank does not have enough loan demand to deploy the funds, and the funds remain on book as lower-yielding cash or securities. Excess deposits negatively impact all asset-dependent ratios, including return on assets, equity to assets, and net interest margin.

So having too many deposits can truly cause issues – banks start to worry about breaching their capital requirements or other regulatory thresholds, and they are faced with falling return on assets, equity to assets, and net interest margin. Interestingly, banks with excess deposits don’t have that many great options. Next time around, we’ll discuss some of the approaches banks take to manage deposit levels.

Best,

Paolo and the ModernFi Team

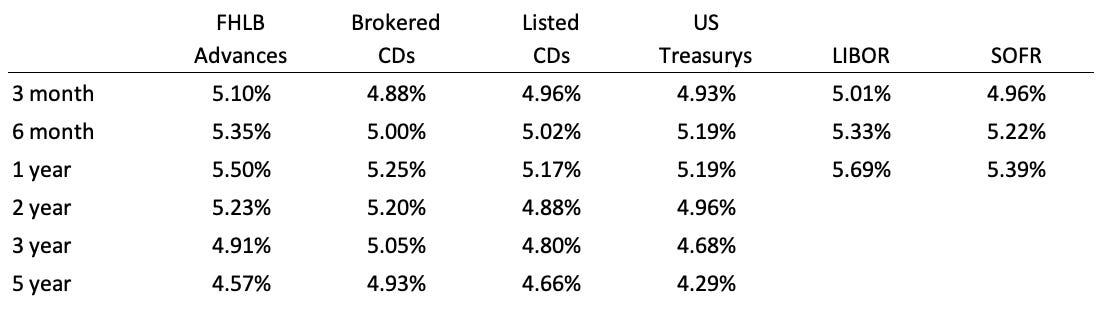

Current rates

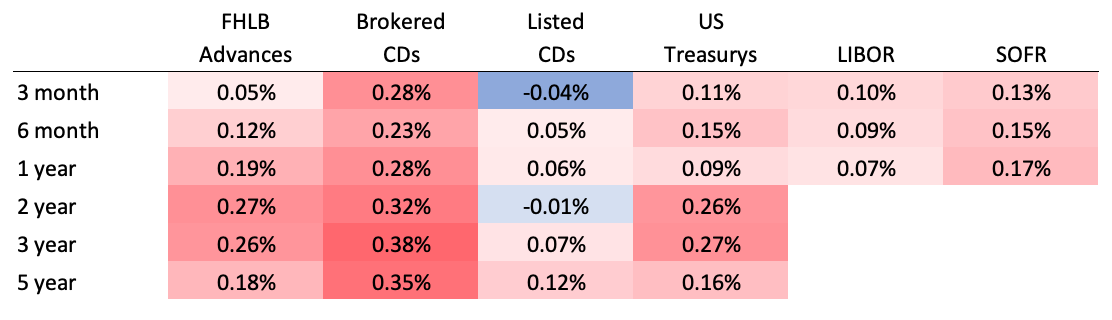

Change from two weeks ago

Sources: FHLB Advances are an average of FHLB Boston, FHLB Chicago, and FHLB Des Moines. Brokered CDs are an average of Fidelity and Vanguard. Listed CDs provided by National CD Rateline. US Treasurys and LIBOR provided by WSJ. SOFR provided by CME.

Disclosures:

All information contained herein is for informational purposes and should not be construed as investment advice. It does not constitute an offer, solicitation or recommendation to purchase any security, and is not intended to provide, and should not be relied on for, tax, legal or accounting advice. Past performance does not guarantee future results. The information contained herein is for institutional use only.

ModernFi Advisers LLC (ModernFi) is not a bank, nor does it offer bank deposits and its services are not guaranteed or insured by the FDIC; ModernFi allocates funds to banks that are FDIC members. ModernFi is an investment adviser registered with the United States Securities and Exchange Commission (SEC). For more information regarding the firm, please see its Form ADV on file with the SEC through the Investment Adviser Public Disclosure website. Registration with the SEC does not imply a particular level of skill or training.

Certain information contained herein has been obtained from third party sources and such information has not been independently verified by ModernFi. No representation, warranty, or undertaking, expressed or implied, is given to the accuracy or completeness of such information by ModernFi or any other person. While such sources are believed to be reliable, ModernFi does not assume any responsibility for the accuracy or completeness of such information. ModernFi does not undertake any obligation to update the information contained herein as of any future date.

Certain information contained herein constitutes “forward-looking statements,” which can be identified by the use of forward-looking terminology such as “may,” “will,” “should,” “expect,” “anticipate,” “project,” “estimate,” “intend,” “continue,” or “believe,” or the negatives thereof or other variations thereon or comparable terminology. Due to various risks and uncertainties, actual events, results or actual performance may differ materially from those reflected or contemplated in such forward-looking statements. Nothing contained herein may be relied upon as a guarantee, promise, assurance or a representation as to the future.

Except where otherwise indicated, the information contained in this communication is based on matters as they exist as of the date of preparation of such material and not as of the date of distribution or any future date. Recipients should not rely on this material in making any future investment decision.